Commenting last week on the publication of the government’s Digital Britain report, RadioCentre Chief Executive Andrew Harrison said that “the devil will be in the detail”. Absolutely true because, sometimes, a single word can tell you more about the direction that government policy is taking than a weighty tome. In the case of DAB, the wording of the Digital Britain report raised one such question: does the government want the DAB platform to supplement FM/AM radio, or does it want DAB to supplant it?

The Final Report of the Digital Radio Working Group last December had recommended:

“DAB as the primary platform for national, regional and large local stations” [emphasis added].

However, last week’s Interim Report of Digital Britain made a commitment:

“to enabling DAB to be a primary distribution network for radio” [emphasis added].

This may seem like an insignificant detail but, for the radio industry, it certainly is not. If DAB is to be the primary platform, the implication is that if your radio station is not available on the DAB platform, your business will be marginalised. It implies that the FM and AM platforms will be closed down, which would be a disastrous outcome for smaller commercial radio stations who may not be able to afford the cost of DAB transmission and/or who cannot find space on their local multiplex (if that multiplex even exists) [see ‘Committed to its listeners’].

On the other hand, if DAB is to be a primary platform, the implication is that it will be available to consumers as an adjunct to existing FM/AM radio and to IP-delivered content. In this scenario, the ideal radio receiver of the future will be one which, to the user, is ‘platform neutral’ but has capabilities to receive DAB, FM/AM and IP. The user would simply select “Radio 4: live” on the radio’s interface and the radio itself would determine which was the most reliable delivery platform in that location to serve Radio 4 live. Or, the user might select “Radio 4: The Archers” and it would deliver the most recent episode by IP.

Strangely, the subtle difference between “a” and “the” seemed to be ignored by some stakeholders:

Laurence Harrison, director of consumer electronics at Intellect, said:

“This commitment to DAB as the primary distribution network for radio is exactly the sort of strong and decisive leadership we wanted to see from government” [emphasis added]

Frontier Silicon, in its first press release:

“…..welcomed the Government’s commitment to DAB as the primary distribution network for future radio broadcasting in the UK” [emphasis added]

Frontier Silicon, in a second press release:

“…..the Government’s endorsement of the digital migration of radio and commitment to DAB as the primary distribution network for future radio broadcasting” [emphasis added].

The precise wording was also reported badly by some media:

The Guardian’s Media Monkey wrote:

“….DAB radio was the ‘primary distribution network’ for radio….” [emphasis added].

The Sunday Times wrote:

“….DAB digital technology, set to become the ‘primary distribution network’ for radio….” [emphasis added].

The Daily Mail wrote:

“Lord Carter, the Communications Minister, said: ‘We are making a public commitment to DAB as the primary distribution medium’…” [emphasis added].

The Telegraph wrote:

“The Digital Britain report…… gives a firm commitment to digital radio (DAB) as the primary way of listening to content in the future” [emphasis added].

The BBC wrote:

“The culture secretary said digital audio broadcasting (DAB) will become the ‘primary distribution network’…..” [emphasis added].

No wonder the public is confused. The potential implication of the Digital Britain report on areas of the UK where DAB reception is presently non-existent is just starting to be realised. “FM reception in Eden Valley may disappear” said one local Cumbria newspaper headline yesterday. More coverage like this will inevitably follow.

How many civil servants must have scoured the precise wording of the Digital Britain report before it was published? The change of emphasis from “the” to “a” is unlikely to have been accidental. If the DAB platform were to fail (no acceleration in consumer take-up, no increased exclusive content), then the government will find it needs a ‘get out of jail free’ card. The word “a” provides it with the perfect caveat, next month, next year, whenever.

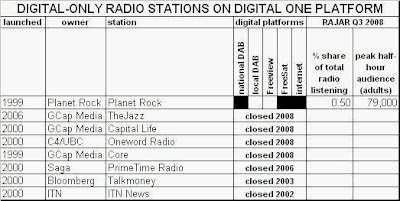

It hardly inspires confidence in the Digital One DAB platform that Global Radio’s predecessor, GCap Media, closed three of its own digital-only stations carried on its platform last year, and sold Planet Rock to an entrepreneur with no other radio interests. Neither is it a good advertisement for Digital One that its

It hardly inspires confidence in the Digital One DAB platform that Global Radio’s predecessor, GCap Media, closed three of its own digital-only stations carried on its platform last year, and sold Planet Rock to an entrepreneur with no other radio interests. Neither is it a good advertisement for Digital One that its